Monopoly

A monopoly (from the Greek monos, one + polein, to sell) is when a product or service can only be bought from one supplier for a specific market. If other firms serve the market, they may be too small compared to the largest, thus allowing the large firm to have a lot of market power. A monopoly usually happens when there is no economic competition to produce the product or service and there is no available substitutes to the product or service.

In economics, a monopoly is a single producer of a product or service. In law, a monopoly is a firm that has a lot of market power and is able to charge very high prices for a product or service. As long as the firm has a lot of market power, it does not matter if the firm is large or small, as size is not used to decide if a firm is a monopoly.

A monopoly can be formed by the government, by merging a few firms to form a large one, or form naturally to become a natural monopoly. In many places, utilities such as telephone service or cable television are monopolies, as it is very costly to build the infrastructure for another firm to compete in the market. Such natural monopolies is hence allowed by the government, but is usually strictly controlled to prevent the monopoly from charging a very high price for a product or service.

Many countries, including the United States, have laws to stop companies from having a monopoly or to limit the actions that they can do as a monopoly.

Features of a monopoly

[change | change source]In classical economics, a monopoly does this:

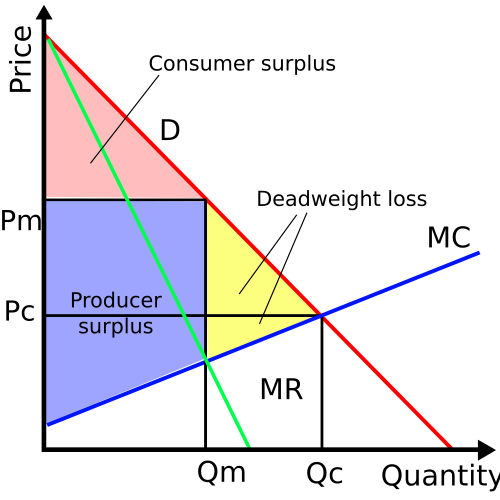

- Profit maximization: Just like any other firm, a monopoly tries to make their profits as big as possible and will produce an output where the marginal revenue and marginal cost curves meet.

- Price setter: With a strong market power, the monopoly is able to set prices for their output based on the demand and supply of the market.

- High barriers to entry: There are things that stop other firms from entering the market. These things can be either "natural barriers" or "artificial barriers".

Monopoly model and efficiency

[change | change source]

A monopoly is a type of firm that wants to make its profits as big as possible, and as the market does not have any other large firms, the monopoly is able to set prices on their products or services. Hence, the monopoly would set a price that would maximize the profits that they gain, but cause the consumers to have to pay more for the same good.

For all types of firms (including monopoly), firms make their profits biggest at the output level in which the marginal revenue and marginal cost curves meet, known as the profit maximizing output. But when a firm is a monopoly, the price that the firm sets is the price level of the demand curve for that amount of output. However, it is better for society if the output level is when the marginal cost and the demand curve meet, which is of a higher output and a lower price than what the monopoly produces. Hence, since society could be better if more of the good is produced, a deadweight loss is created. A monopoly is hence not allocatively efficient.

Depending on the total cost that the monopoly has, a monopoly may be able to earn supernormal profits in the long run. This thus allows the monopoly to have money to do costly innovation or become more cost efficient in producing the products or services. However, there are people who believe that a monopoly may become complacent and not do innovation at all as there is no competition in the market.

Natural monopoly

[change | change source]A natural monopoly can happen when there is very high barriers to entry that it is not profitable for more firms to enter the market for the level of demand that is present in the market. A natural monopoly keeps getting increasing economies of scale for the level of demand in the market, and relatively high fixed costs.[1] The average cost of production would then keep decreasing for the whole demand of the product or service.[2] It is thus cheaper for a single firm to produce the product or service, as it would not be profitable for two or more firms to be in the market.

A natural monopoly is similar to a normal monopoly and can be inefficient. Hence, governments tend to make laws that controls what the natural monopoly does, mainly to set prices at an affordable level.[3]

Related pages

[change | change source]References

[change | change source]- ↑ Binger and Hoffman (1998), p. 406.

- ↑ Samuelson, P. & Nordhaus, W.: ''Microeconomics'', 17th ed. McGraw-Hill 2001

- ↑ Samuelson, W; Marks, S (2005). Managerial Economics (4th ed.). Wiley. p. 376.

| Different Market forms |

|---|

| Perfect competition • Monopolistic competition • Oligopoly • Oligopsony • Monopoly • Natural monopoly • Monopsony |